DoorDash Never Made Any Sense To Me

a grossly unprofitable business, where it's headed, and why you should always tip your drivers

The $40 Billion Company

DoorDash never made any sense to me.

In 2018, DoorDash ended the year with a $204 million loss, even though they brought in $291 million in revenue. Last year in 2022, DoorDash posted an astounding $1.4 billion loss, despite their $6.5 billion in revenue. When you look at the five year period of 2018 - 2022, the company lost a combined total of $3.1 billion dollars. Even with these losses, DoorDash is still valued at $40 billion.

These tremendous losses also come with tremendous revenue growth, which is why the company is so appealing to many. DoorDash saw a 20x increase in revenue over a five year period, from $291 million in 2018 to $6.5 billion in 2022. It comes at a high cost, but they’re rapidly capturing market share, expanding locations, and gaining loyal customers. They owned roughly 65% of the food delivery market in 2022, with the next-in-line giant being Uber Eats at only 25%. For a company that owned less than 10% of the market in 2017, DoorDash has done a laudable job in their expansion, marketing, and advertisement.

The margins are razor thin, but if you can manage to pull even a 1% profit margin while continuing to multiply revenue numbers, you have a business worth building. The real question is can they find that razor thin margin over the next few years?

Unit Economics, Driver Pay, and Restaurant Fees

DoorDash’s viability as a company is incredibly dependent on how well they pay their drivers, how much they pay the restaurants they’ve partnered with, and how willing consumers are to pay a fee for their delivery. This brings into question the unit economics of the company. Back in 2020 when DoorDash went public and filed their S-1 form, they published a cost breakdown on a theoretical $32.90 marketplace order.

Of those $32.90, DoorDash pays the driver $7.90, and pays the restaurant or merchant $20.10, keeping about $4.90 for themselves.

Out of the driver’s $7.90 in earnings, $3.30 of that comes from the tip paid by the customer. This means that the driver’s base pay for this order would only be $4.60, so ~40% of the driver’s pay is coming from tips. DoorDash, obviously, does not advertise their pay model to consumers so as to not look bad, which often unknowingly places the burden of a drivers livelihood on the hands of the customer.

If we look at that $32.90 order from what was published in 2020, only about 14.8% of it is kept by DoorDash, this is also known as the take rate. In Q3 of 2023, DoorDash’s take rate was 12.9% of the total value of its orders, this metric has slowly been climbing, which shows that drivers and restaurants are willing to stick around even if DoorDash is taking more of the pie.

With all that being said, the average DoorDash order is ~$30, meaning they keep only about $3.80 per order. Despite the billions that they have in gross order value, they still lose money on a yearly basis.

Where Does The Money Come From

So how are they surviving? There’s a couple answers to this. The first is that they raised an obscene amount of money in the years prior to their IPO in 2020. They raised so much money in fact, and diluted the company so aggressively, that none of the founders own more than 5% of the company individually. While it’s not unheard of for tech founders to own so little, they do tend to own 2-3x that for their own company during an IPO.

Venture Capital

DoorDash went through nine rounds of funding, Series A through Series H (including a Series A-1) between 2013 and 2020. Their last six rounds of funding EACH raised over $100 million. The Series C to Series H rounds raised $128M, $539M, $250M, $408M, $600M, and $429M respectively. While they were private, they managed to raise just about $2.4 billion. That is insane. They even had to raise money into funding rounds that brought their valuation down. Remember in the early days of DoorDash when nearly every restaurant was buy one get one free or 30% off or free delivery? You have venture capital money to thank for that, they were funding your meals! Every time one of those discounts hit, the money was coming out of DoorDash’s funds, which they could afford from those $2 billion in financing.

In fact, there were even restaurants that took advantage of their own deals. The owner of AJ's NY Pizzeria in Kansas found a brilliant arbitrage opportunity within his own pizzas. A cheese pie that he would sell for $24 was listed on DoorDash’s app for $16. Whenever a customer ordered, they would pay $16 to DoorDash, and DoorDash would cover the difference, paying an additional $8 directly to AJ’s Pizza. The owners had the idea of ordering their own pizzas to themselves, since one third of it was subsidized by DoorDash. They would order pizzas with nothing on them, no cheese, no sauce, literally just dough. With each pizza, they’d make an additional $8 in profit, money that came straight from Softbank. They did this about 10 times in one day, mostly for the fun of it and as an F-you to DoorDash. DoorDash never caught on, I wouldn’t be surprised if there were other restaurants across the country that caught on.

IPO

Their biggest chunk of change came on their IPO in late 2020. DoorDash raised $3.4 billion, with the stock opening up 86% above its IPO price. All that cash obviously serves as a cushion to their recent and tremendous losses. It was the IPO craze of 2020, and investors were eager to jump in.

On a smaller note, they also have a $400 million revolving credit facility that they have access to.

Despite all the cash, it’s not all rainbows. DoorDash stated in Risk Factors section of their latest quarterly report:

We have incurred net losses in each year since our founding, we anticipate increasing expenses in the future, and we may not be able to achieve, maintain, or increase profitability in the future. We incurred a net loss of $295 million and $73 million in the three months ended September 30, 2022 and 2023, respectively, and, as of December 31, 2022 and September 30, 2023, we had an accumulated deficit of $3.8 billion and $4.9 billion, respectively. We expect our costs will increase over time and our losses to continue as we expect to invest significant additional funds towards growing our business. We have expended and expect to continue to expend substantial financial and other resources on developing our platform, including expanding our platform offerings, developing or acquiring new platform features and services, acquiring and integrating technologies and businesses, expanding into new markets and categories, and increasing our sales and marketing efforts. These efforts may be more costly than we expect and may not result in sufficient increased revenue or growth in our business to offset such costs. Any failure to increase our revenue sufficiently to keep pace with our investments and other expenses could prevent us from achieving, maintaining, or increasing profitability or positive cash flow on a consistent basis. If we are unable to successfully address these risks and challenges as we encounter them, our business, financial condition, and results of operations could be adversely affected.

In the Liquidity and Capital Resources section they stated:

We have generated significant operating losses from our operations as reflected in our accumulated deficit of $4.9 billion as of September 30, 2023. To execute on our strategic initiatives to continue to grow our business, we may incur operating losses and generate negative cash flows from operations in the future, and as a result, we may require additional capital resources. We believe our existing cash, cash equivalents, and marketable securities, along with the $400 million in available borrowings under our unsecured revolving credit facility, will be sufficient to meet our working capital and capital expenditures needs for at least the next 12 months and beyond.

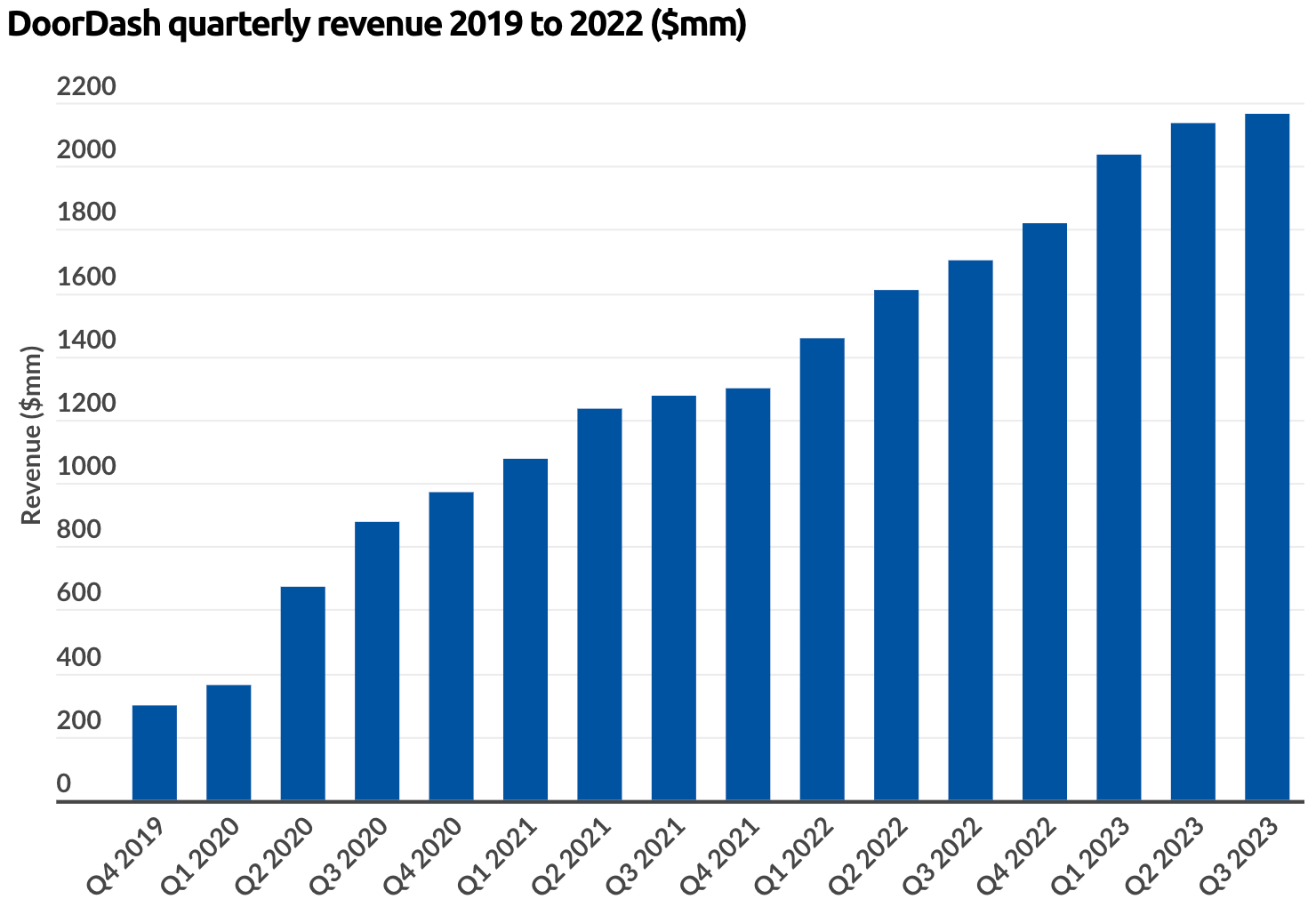

Scary to read, especially when they’re seemingly so far from profitability! The last thing worth mentioning here is that DoorDash brings in an obscene amount of revenue and revenue growth. Here’s their quarterly revenue going back to 2019:

Year-to-date for September of 2023, DoorDash was sitting on $6.3 billion in revenue. They burn a lot of money, but it sure does help that they’re seeing the exact growth they’ve been trying to buy.

Final Thoughts

While I’m not a fan of DoorDash given it’s tremendous losses, driver scandals and lawsuits, and lack of a clear path to profitability, it’s undeniable that it’s wiping away its competitors. While the economics of the company don’t quite make sense yet, it’s clear that a market for food delivery needs to exist. Consumers have grown used to ordering in and restaurants hate being on the phone taking delivery orders. The market is there, and DoorDash has far and beyond been the most successful over the past few years. Of course, the success comes at the cost of billions of dollars lost. Capturing the market share, however, has been undoubtedly “worth it” in the eyes of many investors. There are three reasons for this.

Loyalty

The first is customer loyalty. The choice to use DoorDash over Postmates or Uber Eats or whichever other food delivery app is huge. DashPass is a great example of this, showing that dedicated customers will almost certainly be recurring users on the platform. In 2022, DoorDash reported 15 million subscribers to the service. At $10 a month and under the assumption that those members will remain subscribed, 2023 can expect a revenue in the hundreds of millions brought in from DashPass. This too comes at a cost, which is that there are less upfront fees for DoorDash to collect in any given DashPass order. It does, however, guarantee cash and build loyalty — the DoorDash market share will continue to grow if they play this correctly.

Eyeballs and Advertisements

The second reason ties into the first. If they have market share, specifically loyal market share, that means that they have eyes on their platform. In 2022 DoorDash had 32 million active users. It’s the perfect contender for a robust advertising business. They already have an advertising arm, a very low cost business to help push them into profitability. This is profitable, but it’s frustrating. It’s frustrating because, as the business currently stands, the dashers are getting screwed. It’s likely they won’t be given a bigger piece of the pie, and it feels like an advertisement business would be used to fund the cheap labor of drivers — whose pay already falls on the backs of the customers through tipping.

Amazon Prime

The third reason that spending so much money has been worth it is because of the scale at which they can build at, given so much market share. Amazon Prime comes to mind. DoorDash will try to pull off evolving into an Amazon Prime 2.0, where anything you want delivered at any given moment will arrive at your doorstep. Not through two-day free shipping, but through a 45 minute delivery driver that will likely not make enough money for the convenience they are providing. DoorDash banks on the fact that if they can logistically deliver ice cream to your door before it melts, then they can theoretically deliver anything that fits in a driver’s trunk.

Lastly

Despite ending on an ideologically bullish note, DoorDash still doesn’t make sense a whole lot of sense to me. Maybe it’s just a moral quandary sitting inside my stomach knowing that even if they manage to turn a profit, the pay of the dashers will continue to burden the customers. Maybe it’s unfounded. This whole gig economy is made up of people, the economy is made up of people, it’s important to make sure we’re treating these people well.

Thanks for reading, thanks for your time. I hope you’re doing well.

Lucas