Fiscal Dominance: An Interest Rate Paradox

what is policy, fiscal vs monetary, and the recession button

If you enjoy my writing, please consider subscribing! It’s free AND fun.

What Is Policy

I want to paint a picture of the economic situation that the United States finds itself in — one of fiscal dominance. To understand the underpinnings of the economy right now, we need to understand the two policy mechanisms by which the United States influences the economy:

Monetary Policy

Fiscal Policy

Monetary Policy

Monetary policy is the responsibility of the Federal Reserve (aka the Fed) — a quasi governmental institution — in order to influence the money supply and hopefully achieve economic growth. The Federal Reserve has a dual mandate to (1) achieve maximum employment and (2) keep prices stable. Ideally, the Fed leverages its toolkit such that the maximum employment leads to economic growth while not overheating the economy and de-stabilizing prices (i.e inflation). It’s a delicate balance between the two. For example, if unemployment is very low and wages are very high, then the economy might be great but it might also get too hot if people spending too much money, which then can lead to inflation.

The primary tool that the Fed has for influencing monetary policy is the interest rate that it sets, which is known as the Federal Funds Rate. You can think of the FFR as the interest rate at which banks lend to other banks, and as a result, it becomes the “base” rate at which a bank lends out money — it effectively sets an interest rate floor. The Fed Funds Rate has great influence over all the other interest rates that rule the economy — bank rates, mortgage rates, credit cards rates, etc. The easiest way to think about this is to think about mortgage lending. When the Federal Reserve lowers the Fed Funds Rate, that subsequently lowers mortgage rates. When mortgage rates are lower, people are more likely to buy homes. When you have a lot of people buying homes, it is stimulating to the economy because it suggests people are spending money, building housing, hiring contractors, buying furniture, and thus more money is circulating in the economy. Here’s a graph on the Fed Funds Rate versus the average 30-year fixed mortgage:

Mortgage rates are heavily influenced by the Fed Funds Rate, as is every other interest rate you can think of for the most part.

To reiterate — raising and lowering the Fed Funds Rate is the Fed’s primary tool for enacting monetary policy decisions. The direction that they take the FFR heavily influences bank lending in order to stimulate or cool down the economy. If inflation is running hot because banks are lending too much money, thus pushing the money supply up which raises prices, then the Fed can increase interest rates to discourage borrowers from taking out loans, as it would now be more expensive to do so. That’s monetary policy in a nutshell. There are some other tools that the Federal Reserve employs, but I think just discussing interest rates will do for now.

Fiscal Policy

Fiscal policy is a bit easier to understand and create a mental model for. It refers to the government spending money in order to influence economic conditions and ideally sustainably grow the economy. The money to pay for fiscal policy comes from (1) the taxpayers and (2) the debt that the government raises in the form of bonds. Because the government spends more money than it takes in, it has to fill the gap by issuing bonds, which is econ speak for borrowing money from anyone who is willing to lend it to them. Fiscal policy ranges from lowering taxes to building highways to providing stimulus checks, and generally needs to be funded additionally through debt.

The past few years, we’ve seen a TON of fiscal packages get passed — the American Rescue Plan, the Infrastructure Investment and Jobs Act, and the Inflation Reduction Act. These are all examples of fiscal policy, where the government injected money into the economy in order to stimulate it. The recovery that the United States had during the COVID years was really great when compared to other first world countries, and these examples of fiscal policy were certainly one of the main drivers of that recovery. With that being said, we also saw inflation levels not seen in 40 years, largely because there was so much new money finding its way into the economy, raising prices across the board (and supply shocks from COVID, of course). This is the “money printing” that people like to throw around. The treasury department will issue new bonds, and the Federal Reserve will purchase those bonds with new money it can create. This is known as monetizing the debt.

Policy Takeaway

The main takeaway from the above policy overviews is that both fiscal policy and monetary policy can be used to affect the amount of money in the economy. The former does so by heavily influencing bank lending through interest rate control, and the latter does so by directly injecting taxpayer dollars and debt into the economy. When done strategically, both policy methods can act as engines of growth. However, if one or both levers are pulled too hard, the result can be inflationary for the economy. That’s effectively what we saw the past few years. Monetary policy drove interest rates to zero, while fiscal policy sent stimulus checks to most Americans. This was all done in the name of stimulating the economy in a time when business were shutting down and people were out of work. But it’s a sensitive scale that, when tipped too far, can drive prices up.

When Fiscal Policy Overshadows Monetary Policy

Now that we understand what fiscal and monetary policy are, we can dive into why we are in a period of fiscal dominance right now.

When debt and deficit levels for a country are very high, as they are now in the United States, monetary policy can take a backseat in influencing inflation, while fiscal policy takes center stage. Why does this happen?

If inflation is running hot, typically the Federal Reserve will orient its monetary policy by raising interest rates. However, when a country is so ridden with debt, raising interest rates also raises the cost of servicing that debt, which will push deficits even higher and force the government to print even more money. What does this look like? The United States is $36 trillion dollars in debt. Right now, it costs about $800 billion dollars a year to service that debt i.e to pay the interest out to the bond holders. Because we are so indebted, when our interest rates go up, the cost to service the debt goes up, and we have to borrow even more money to pay our obligations.

The classic debt spiral. We’ve seen this in many countries — Argentina, Venezuela, Greece, etc.

In cases like this, interest rate control can be ineffective in achieving its intended purpose of reigning in inflation. The best way to think about this is that since the creation of the modern economy, growth is almost always driven by two factors:

Private sector wealth creation

Government spending

The reason we have two main policy tools, fiscal and monetary, is because they can create rules for how private sector wealth creation and government spending should behave. In the era we are in now, government spending overshadows the private sector, and thus fiscal policy overshadows monetary policy.

Lyn Alden has some great charts on this:

Here, we can see the deficit growth against bank loans, and up for many decades we saw bank loans greater than the deficit increase. That was a time when monetary policy would have been a great tool.

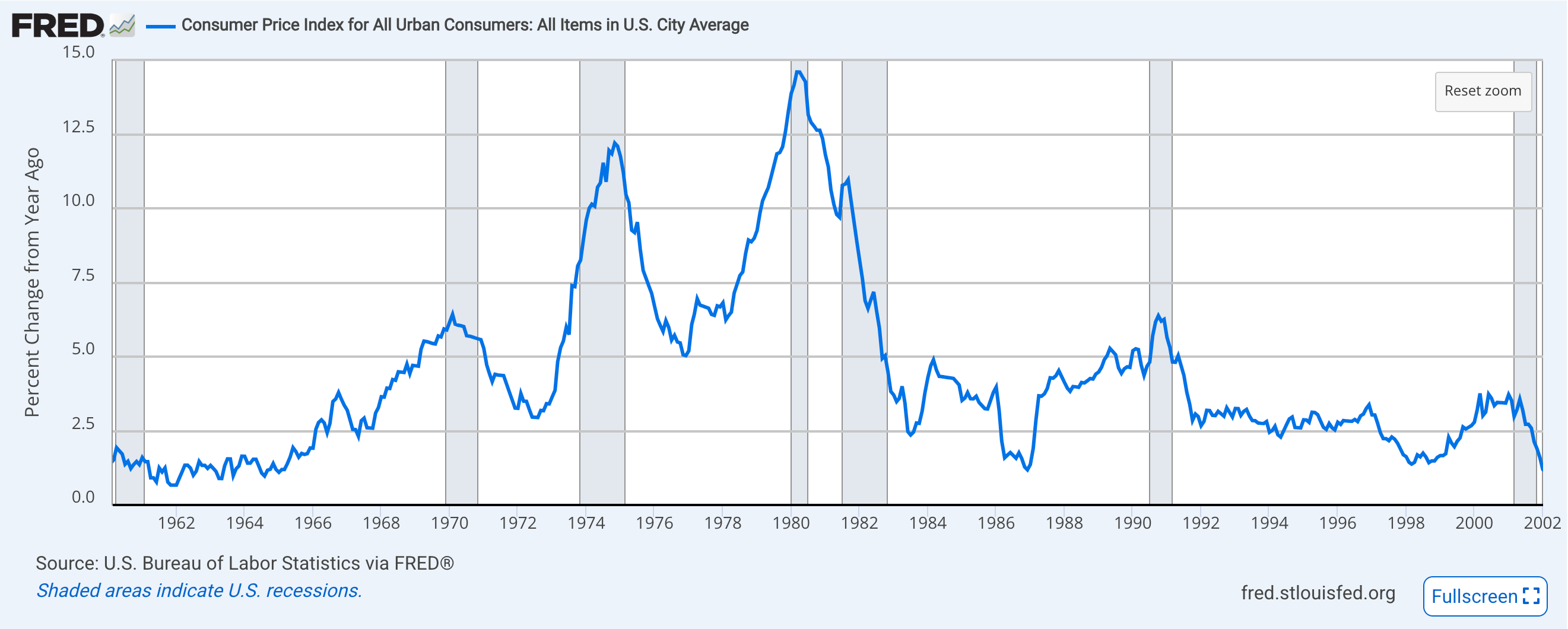

The 1970’s

A great counter-scenario to where we find ourselves today is the 1970’s decade. Inflation reached as high as 14%, but under very different conditions than the current day and age.

This was not a fiscally dominant era, it was a monetary dominant era, and thus interest rates served as a great tool for influencing inflation. At the time, baby boomers were coming into their prime working years, having kids, buying homes — the United States witnessed a private bank lending boom. People needed mortgages, they need business loans, and generally they relied on banks to provide those loans to them. And provide they did. The private sector pulled its weight and pushed the economy, but the result from all the money creation through loans was inflation.

In this period, Paul Volker, then chairmen of the Fed, raised rates aggressively and eventually reigned in inflation. But the solutions then are not the most applicable now, as we are in such a fiscally dominant environment.

Where are we today? The Recession Button

Fiscal dominance comes down to the deficit. The higher the deficit, the more fiscal dominance we’ll see. Committees such as DOGE, which I’ve written extensively about, were created to tackle this deficit problem. But realistically, DOGE won’t make a dent in the deficit given how much of it is allocated towards mandatory spending like social security, medicare, and medicaid.

And literally not a single cent cut by DOGE matters in the slightest when all the spending cuts are being offset by a bazooka of tax cuts for the wealthiest people in the country.

Alongside all the chaos, it seems like President Trump has pushed the recession button. He slashed public service jobs, started a trade war, tariffed our allies, and more. The Atlanta Fed’s GDP predictions have dropped like a stone. One month ago, they were projecting +3.9% growth, and now they’re expecting a -2.8% contraction. I mean, that’s insane.

Consumer spending has fallen as people grow more and more worried about the state of the economy and imports have skyrocketed as companies want to ensure they can lock in good rates on their products prior to the tariffs kicking in.

It seems like all things point to eventual rate cuts. Treasury Secretary Bessent has stated in several interviews that he wants to see rates drop (not necessarily from the Fed, but from the market as a whole). If interest rates were to fall, the question becomes whether or not the drop in interest rates offsets inflation due to the drop in net interest expense, or if it exacerbate inflation by further encouraging lending. It’s too big of an unknown for me to attempt to answer, but interest rates certainly seem like the wrong north star.

The priority shouldn’t be to lower rates and then figure the rest out — especially if lowering rates comes at the cost of nuking the economy. We need to remember that the economy is comprised of people. People who rely on global trade and government programs and government jobs and grants and more. The economy exists for those people — it’s not the people that exist for the economy. It’s an important distinction, one we’re losing sight of I think.

Thanks for reading and I hope you’re doing well.

- Lucas